Stop Trading These 10 Leveraged ETFs Built to Lose

Wall Street is very good at giving traders exactly what they think they want—and charging them for what they don’t understand.

Leveraged ETFs can make you feel like you’ve found a shortcut. But the problem with shortcuts is that if they really worked as easily as advertised, they wouldn’t be shortcuts — they’d be the way.

I’m sure many of you have traded them before. And if we’re being honest with ourselves… you might even have liked trading them.

They move.

A lot.

And that’s exactly the problem.

Let me explain…

The Product Everyone Loves… for the Wrong Reasons

When you buy a leveraged ETF, you’re not buying the stock.

You’re buying a daily-reset derivative designed to give you a multiple of that stock’s daily move.

Two times. Three times. Sometimes more.

And that word—daily—is everything.

Because every single day:

- The fund resets

- The exposure recalibrates

- The math starts over

It doesn’t care about your thesis, where the stock was last week or what your entry price is.

It just resets.

And then it compounds from there.

Why Professional Traders Don’t Use Them

I started Masters in Trading back in 2015.

Before that, I spent decades on the professional side of this business — CME floor, prop firms, market making at the CBOE. I was managing risk, trading size, thinking in terms of structure, probabilities, positioning.

And here’s the honest truth…

Leveraged ETFs were not a core part of my world.

Not because they didn’t exist — but because the way professionals think about exposure, we don’t need them.

If I want more leverage, I size up. Defined risk? I use options. If I want precision, I build the trade myself.

So when I started working more directly with individual traders, I was surprised to find so many of these poorly structured products getting buzz among my readers.

Why Traders Gravitate Toward Them

It’s not hard to understand.

You pull up your scanner, you see a name like AXT Inc. (AXTI) lighting up with unusual options activity… and then right behind it, someone launches a 2x version of it, enter Tradr 2X Long AXTI Daily ETF (AXTX).

Of course they do. The thought of doing something twice as fast has a lot of appeal, which means people are going to give them what they think is more of a good thing.

If traders are chasing volatility, Wall Street is going to package that volatility and sell it right back to you — with leverage.

And when you trade these products, you’re buying the promise of getting more gratification, faster.

That’s why certain trading cliques love them.

They feel exciting.

But there’s something baked into these products that most people don’t understand…

They leak.

And I don’t mean metaphorically.

I mean structurally.

They are designed in a way where — over time — you are fighting against the math.

The Part They Don’t Want You to Notice

Let me give you the simplest example.

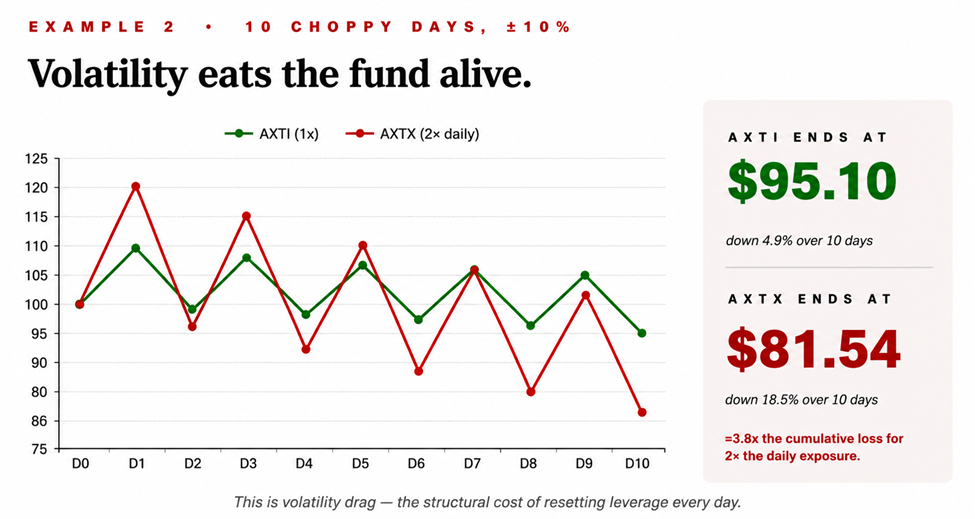

Imagine a stock goes up 10% one day and then gives it right back the next day, down 10%. Most people instinctively think, “Alright, I’m back to even.” But you’re not—you’re actually down a little bit, about 1%. That’s just how percentages work.

Now take that exact same path and apply a 2x leveraged product to it. Instead of up 10%, you’re up 20%. Instead of down 10%, you’re down 20%. And now, instead of being down 1%, you’re down closer to 4%.

Same underlying move. Same two days. Completely different result.

That gap — that widening loss — is what traders call volatility drag or volatility decay.

The more volatile the path — meaning the more frequent and larger the swings up and down — the more those small losses begin to accumulate.

Over time, that creates a measurable gap between the asset’s starting point and its ending value, even if the price appears to be moving sideways overall.

Here’s what that looks like over ten days of back-and-forth movement where the stock itself finishes only slightly lower. It doesn’t look dramatic at first glance…

But the leveraged ETF? It’s down big.

Same underlying move. Wildly different outcome.

That’s not bad trading or poor timing.

That’s the structure of the product quietly working against you the entire time.

Now Layer Options On Top of That…

This is where the situation becomes more complicated. At this point, you’re no longer dealing solely with the standard dynamics of options like time decay and changes in implied volatility — you’re also working with an underlying product that is structurally losing value over time.

Options have the wonderful ability to amplify small moves in underlying equities. It can turn a small gain into triple-digit returns, and big gains into windfalls.

But when you try to amplify products that are built to lose, you end up amplifying that loss more often than not.

You’ve added another layer of friction to your trade before it even has a chance to work.

So even if you’re right on direction… even if the move you’re anticipating eventually plays out… the trade can still disappoint. And that’s where a lot of traders get tripped up.

It feels like the timing was off, or the market didn’t cooperate, when in reality the vehicle itself is working against you the entire time. You’re not just trying to be right—you’re trying to overcome multiple headwinds at once.

That’s why I say this very clearly: if you’re trading options on leveraged ETFs, you’re pushing a boulder uphill. It doesn’t mean it’s impossible. You can absolutely make money doing it. But you’re making the job harder than it needs to be, and over time, that added difficulty has a way of showing up in your results.

How We Turn Opportunity Into a Structured Trade

A good way to understand this is to look at a setup where you’re not layering complexity on top of complexity — you’re working with a clean underlying and using options the way they’re intended to be used.

In our recent trade on POET Technologies Inc. (POET), we’re dealing with a single stock.

No daily resets, embedded leverage, or structural quirks underneath the surface.

So when we add options to that position, we’re not compounding hidden risks—we’re simply enhancing the exposure.

The options are directly tied to the stock’s movement, which means if the stock moves in our favor, the options respond cleanly to that move. There’s no distortion in the relationship, no extra variable quietly working against us in the background.

We kept things simple: One underlying, one directional thesis, and a defined-risk options structure layered on top.

So instead of fighting multiple headwinds — time decay, implied volatility, and the behavior of the product itself — we’re focused on one thing: whether the stock moves.

And when it does, the structure is designed to pay you, not work against you.

When it was all said and done, our call spread reeled in a 492% return from an 80% move in the stock in 74 days.

That’s what alignment looks like. And that’s why this type of setup tends to produce more consistent, repeatable outcomes over time.

Trades like POET aren’t one-offs. It’s a repeatable process — from identifying setups, structuring the position, and managing the trade once it starts working. These are the fundamental elements of options trading we focus on inside the Masters in Trading Challenge.

Over the course of just seven days, I lay out the framework you can apply over and over again so that when the market presents an opportunity, you know how to act on it. If you want to see how this comes together in real time—and start applying it yourself—you can learn more about the Masters in Trading Challenge here.

This is the standard I want you using when you evaluate an options trade.

Is the underlying clean? Does it have clear structure? Is the risk defined? Is the trade giving you a direct way to express the thesis?

Because if the answer is no, I’d rather pass.

And that brings me to the names I see traders reach for all the time — the ones that look active, look liquid, look exciting… but are built on exactly the kind of structure we want to avoid.

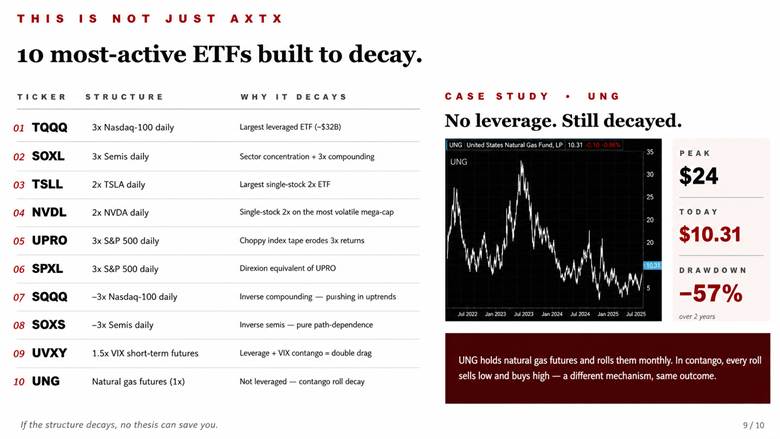

The ETFs I Want You to Treat Like the Plague

These are some of the most actively traded products I see come across our scanners and conversations.

And I don’t want you touching them—especially with options.

TQQQ — ProShares UltraPro QQQ

3x daily exposure to the Nasdaq.

This one looks incredible in a straight-line rally. But in any kind of chop, the decay adds up quickly. If you’re buying options here, you’re stacking leverage on top of leverage—and the math will catch up to you.

SQQQ — ProShares UltraPro Short QQQ

3x inverse Nasdaq.

Pull up a long-term chart. It’s a slow-motion grind lower with constant reverse splits. That’s decay in action.

SOXL — Direxion Daily Semiconductor Bull 3x

3x semiconductors.

Semis are already volatile. Now you’ve added leverage and daily reset mechanics. Great for intraday movement. Dangerous for anything beyond that.

SOXS — Direxion Daily Semiconductor Bear 3x

3x inverse semis.

Same issue as SOXL, just flipped. You’re not just betting against the sector—you’re betting against the structure holding up over time.

SPXL — Direxion Daily S&P 500 Bull 3X Shares

3x daily exposure to the S&P 500.

This one gives traders triple exposure to the broad market, which can look great when the index is moving straight higher. But the S&P 500 doesn’t move in a straight line. In choppy conditions, the daily reset and leverage create volatility drag, and buying options on top of that means you’re stacking leverage on an already leveraged product.

UVXY — ProShares Ultra VIX Short-Term Futures

Leveraged volatility exposure.

This is one of the cleanest examples of decay in the entire market. It exists to trade short-term volatility spikes—not to hold, and definitely not to build options positions around.

UCO — ProShares Ultra Bloomberg Crude Oil

2x oil exposure via futures.

You’re dealing with leverage and futures roll costs. That combination erodes value over time—even if oil trends correctly.

AGQ — ProShares Ultra Silver

2x silver exposure.

Commodities already have their own quirks. Add leverage and daily resets, and you get tracking issues that make options pricing even more difficult to navigate.

SSO — ProShares Ultra S&P 500

2x S&P 500.

Even in a broad index, the same math applies. In a trending market it can work. In a choppy one, the decay quietly eats away at returns.

UNG — United States Natural Gas Fund

Not leveraged—but still decays.

This is an important one.

Even without leverage, the futures structure creates a long-term drag. Add leverage on top of something like this, and it only gets worse.

The Way I Think About It

If I’m bullish on a name, I’ll buy the name.

If I want leverage, I’ll structure it myself — with options and defined risk.

But I’m not going to rent a decaying product that resets every day and expect it to behave over time.

Because it won’t.

And if you take one thing from this, let it be this:

You’re not just trading direction with these products.

You’re trading against the clock…

Against volatility…

And against the structure itself.

That’s a tough game to win, so don’t play it.

The post Stop Trading These 10 Leveraged ETFs Built to Lose appeared first on InvestorPlace.